Tiny Molecules, Tinier Incentives: How the IRA Rewrote the Small-Molecule Economy

Even the strongest science does not guarantee an investable asset. Here, we discuss how to align early-stage discovery programs for small molecules with investor expectations in a complex biotech funding environment.

Tiny Molecules, Tinier Incentives: How the IRA Rewrote the Small-Molecule Economy

By Pranav Seshadri & Kwesi Frimpong-Boateng

Even the strongest science does not guarantee an investable asset. Here, we discuss how to align early-stage discovery programs for small molecules with investor expectations in a complex biotech funding environment.

Chapters

Introduction

Small Molecules: A Cornerstone of Pharmacotherapy

The Inflation Reduction Act

Parallel Pathways, Divergent Futures

On Medicare

T.Rx’s Perspective

Conclusion

Introduction

Small molecules remain central to modern therapeutics, but their commercial landscape has shifted dramatically in the wake of the Inflation Reduction Act (IRA). For Medicare-covered small molecules, reduced effective exclusivity shortens the period in which companies can recoup R&D investment; even a two- to three-year loss in protected revenue can erase billions in forecasted value, reshaping how early development and financing decisions are made. As a result, both biopharma and venture investors have become far more selective about which programs can realistically deliver durable value. In parallel, aggregate investment into small molecules—particularly those targeting Medicare-aged populations—has declined sharply. Yet the modality continues to attract meaningful capital, with $1.2B deployed in the first half of 2025 and an additional $1.4B in licensing and upfront payments. The signal is clear: investors have not abandoned small molecules, but the bar is higher, and the strategy must be sharper.

In today’s environment, strong biology alone is no longer enough. Clinical efficacy must be paired with a credible economic narrative: one that anticipates reimbursement hurdles, pricing pressure, and payer adoption from the outset. Technical success may get a therapy to approval, but commercial viability determines whether an asset becomes acquisition-worthy and whether value ultimately flows back to founders, employees, and investors. Founders who succeed in this climate understand both the constraints and the opportunities of the modality. They design target product profiles that build in differentiation, address market insufficiencies, and reflect a realistic path to defensible, durable value creation.

Here, we explore how T.Rx is evaluating small-molecule strategies today, from where true therapeutic breakthroughs still exist to how early-stage companies can align scientific innovation with commercial logic. We aim to clarify how T.Rx navigates a pressured biotech market where compelling science and compelling economics must work in concert to create value.

Small Molecules: A Cornerstone of Pharmacotherapy

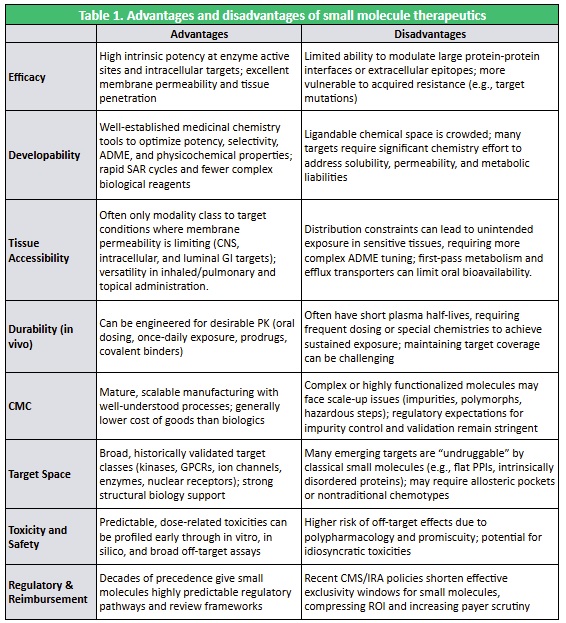

Small molecules, low-molecular-weight organic compounds typically ≤1000 Da, remain one of the most versatile and widely deployed therapeutic modalities in medicine. Their defining advantages stem from their physicochemical properties: oral dosing, membrane permeability, and the ability to reach intracellular targets that biologics cannot (see Table 1). Medicinal chemistry enables systematic tuning of potency, selectivity, solubility, and pharmacokinetics, while mature synthetic chemistry supports rapid optimization and highly scalable, cost-efficient manufacturing.

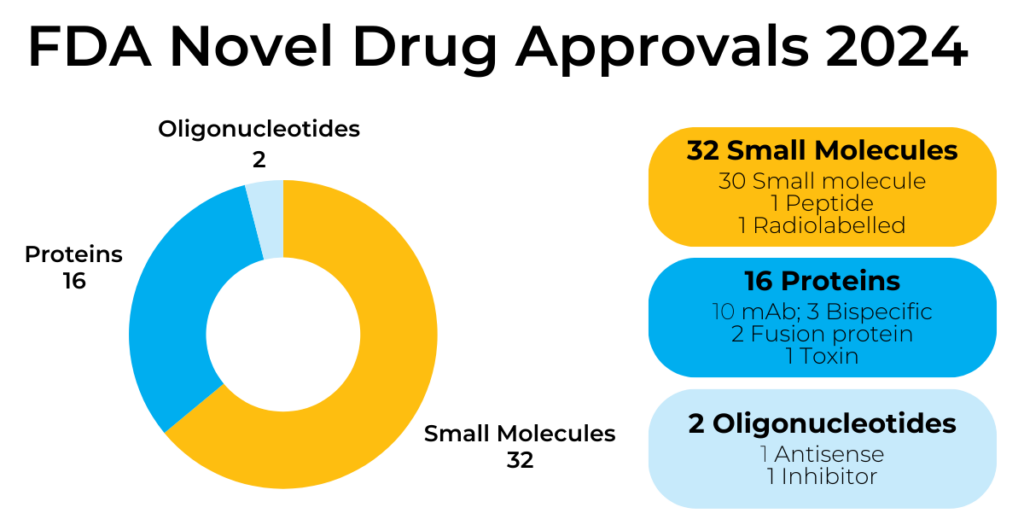

Mechanistically, small molecules modulate enzymes, receptors, and signaling pathways by binding to discrete pockets, enabling precise influence over intracellular biology. This has made them indispensable across therapeutic areas for more than half a century. The trend continues: in 2024, small molecules comprised 64% of the 50 novel FDA approvals (see Figure 1), reinforcing their central role despite the rise of RNA, biologics, and cell and gene therapies.

Fig 1. Small Molecules Comprise the Majority of FDA Novel Drug Approvals

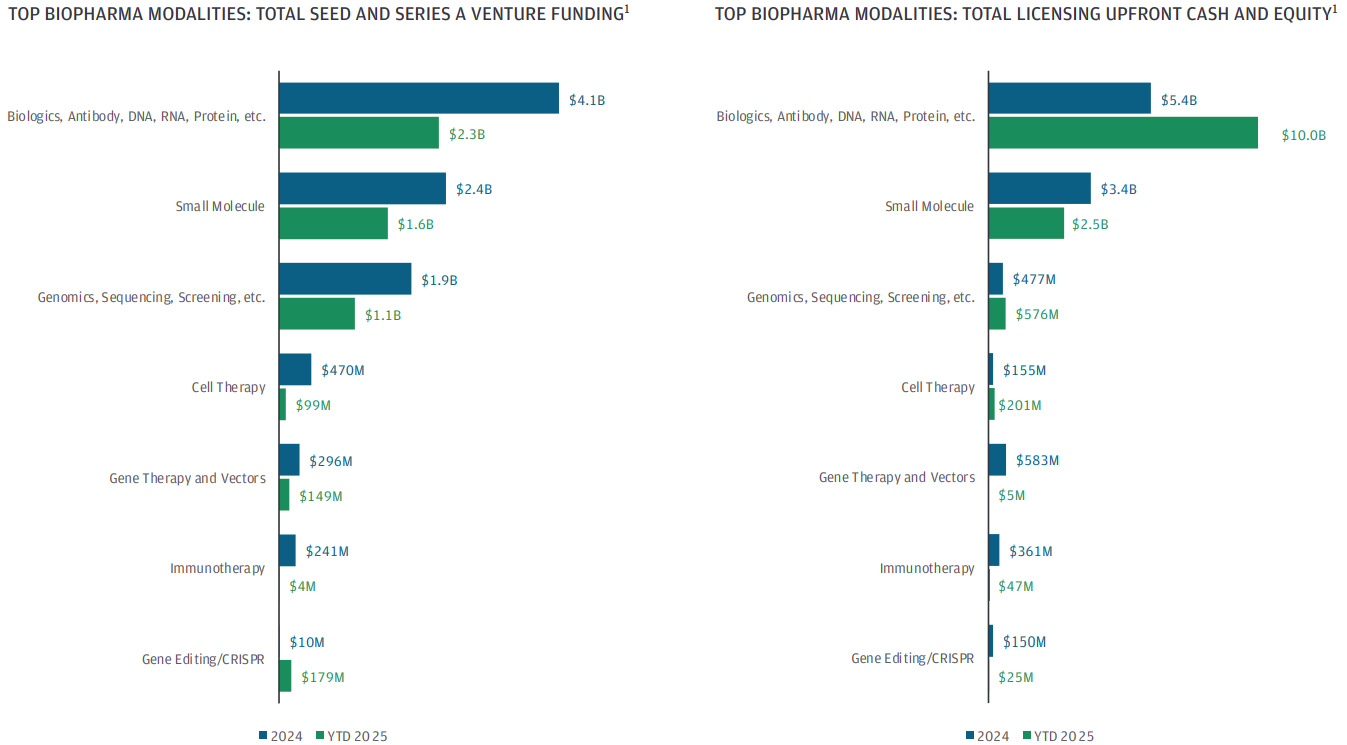

Commercial performance mirrors this scientific utility. Blockbusters like Eliquis, which exceeded $13B in global sales in 2024, demonstrate the revenue potential of well-positioned small-molecule programs. And despite a tightened funding environment, the modality remains resilient: JP Morgan reports that early-stage cash flows into small molecules in 2025 are pacing slightly below 2024 but continue to attract significant investor and strategic interest.

Fig 2. Small Molecules Compete with Biologics Amidst a Biotech Winter

Small molecules therefore remain a core tool in drug development, valued for their broad therapeutic applicability, well-established development and regulatory pathways, and favorable scalability and accessibility. Even as next-generation modalities expand, small molecules continue to offer a uniquely efficient and economically compelling route to treating a wide range of diseases.

The Inflation Reduction Act

Despite the enduring scientific value of small-molecule therapeutics, the modality now faces structurally weaker commercial economics under the Inflation Reduction Act (IRA). The most consequential provision is simple: Medicare may negotiate prices nine years after FDA approval for small molecules, versus thirteen years for biologics. That four-year delta, effectively a 30% reduction in protected revenue time, has meaningfully compressed the net present value (NPV) of small-molecule programs, particularly those targeting Medicare-heavy populations.

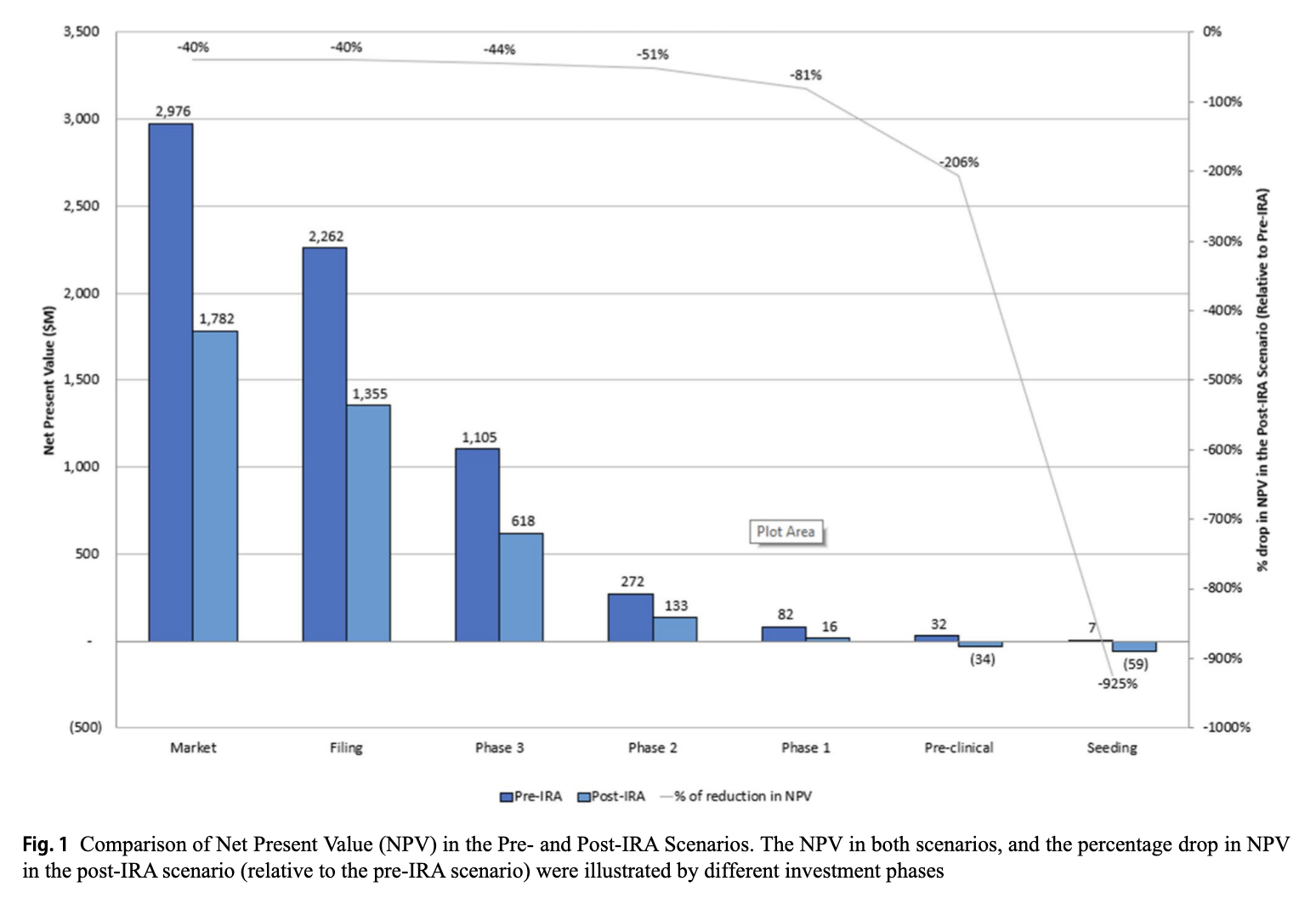

Recent modeling by RA Capital (Xie, Cameron & Kolchinsky, TIRS, 2025) underscores just how steep the economic penalty can be. Using Novartis’ Entresto (one of the first drugs selected by CMS for IRA price negotiation) as a representative case, they show that for programs with significant Medicare exposure, project-level NPV at launch can contract by roughly 40% under post-IRA assumptions (see Figure 3). Notably, this drop occurs even when the underlying science, clinical profile, and market demand remain constant. The only change is the shortened protected revenue window. In effect, the IRA has rewritten the economic baseline for small-molecule development, reshaping how the industry thinks about risk, return, and where capital flows.

Fig 3. Comparison of Net Present Value in Pre- and Post-IRA scenarios, illustrated by different investment phases.

Source: “The Impact of the Inflation Reduction Act on Investment in Innovative Medicines: A Project-Level Analysis” Xie, Cameron, & Kolchinsky (2025)

Capital markets have responded accordingly. Large pharma companies are reweighting pipelines toward biologics, which retain the longer 13-year negotiation runway, and venture funding for small-molecule lead assets has fallen more than 70% since late 2021. The science has not become less compelling, but the economic scaffolding around that science has become less forgiving.

In this environment, the bar for new small-molecule investments is simply higher. Strong biology and validated mechanisms remain essential, but they must now be paired with clear differentiation, a plausible pricing defense, and indication selection that minimizes early Medicare exposure. Investors are still backing small molecules, but only those built with economic durability (and IRA-proofed value creation) in mind.

Parallel Pathways, Divergent Futures

In crowded therapeutic areas, preclinical small molecules must now show a credible path to commercial differentiation from day one. Investors increasingly look for evidence of broader patient reach, monotherapy feasibility, and resistance-resilient biology. Strategics, in parallel, want line-of-sight to multi-indication expansion for maximized early revenue and/or novelty in biology for a stronger IP position. These features meaningfully change the probability of clinical success and the shape of early revenue curves.

A simple illustration comes from comparing two small-molecule inhibitors aimed at the KRAS pathway.

*Note: This table is for illustrative purposes only and is not intended as investment advice, promotion, or solicitation.

NEJM (2021): Awad et al., Acquired Resistance to KRAS G12C Inhibition — https://www.nejm.org/doi/full/10.1056/NEJMoa2105281

An allele-specific inhibitor like sotorasib, which targets only KRAS G12C, is inherently limited to a narrow patient segment and often produces only partial responses, with resistance emerging quickly enough that combination strategies become necessary early in development.

A mutant-selective pan-KRAS inhibitor (e.g., INV-001) designed to hit multiple oncogenic alleles (G12D, G12V, G12R, G12S, G13D) while sparing wild-type KRAS represents a fundamentally different strategic proposition from an allele-specific agent. Broader allele coverage immediately expands the addressable population, and preclinical head-to-head data highlight the practical impact: whereas sotorasib often achieves only partial responses and frequently relies on combinations to manage rapid adaptive resistance, the pan-KRAS profile delivers robust monotherapy activity across diverse KRAS-mutant in vivo models, with deeper MAPK pathway suppression, more consistent tumor regressions, and a delayed resistance trajectory. Together, these attributes form a stronger pharmacodynamic foundation and a clearer path to differentiated clinical and commercial value.

The issue isn’t KRAS in particular. The takeaway is what the comparison highlights. Investors respond quickly to programs with broad utility, solid safety profiles, real monotherapy potential, and mechanisms that curb resistance. These features help counter IRA limits on exclusivity by opening earlier revenue paths, trimming development costs, and strengthening commercial defensibility.

With small molecule economics under pressure, the G12C and pan-KRAS comparison underscores the real benchmark. Scientific originality is only the starting point; what secures investor confidence is differentiation that scales clinically and commercially.

On Medicare

Medicare plays an outsized role in shaping the commercial trajectory of many therapeutics, particularly in oncology and chronic diseases where the majority of patients fall within the 65+ population. Because Medicare is the primary payer for these conditions, its pricing policies, including the Inflation Reduction Act’s negotiation timelines, directly influence the revenue runway and perceived investability of a small-molecule program.

Medicare’s reach is broad:

Part B covers physician-administered drugs (including many oncology injectables).

Part D covers oral and self-administered drugs, where small molecules dominate.

Part A indirectly influences drug utilization through inpatient reimbursement dynamics.

Given that small molecules are disproportionately represented in Part D, they face not only a shorter nine-year negotiation timeline under the IRA (versus thirteen years for biologics), but also the existing friction inherent to Part D access. Step edits, multi-tier formularies, and reimbursement delays can slow early uptake, meaning small-molecule programs must demonstrate value earlier and secure meaningful adoption well before price negotiations begin.

But these constraints do not make small molecules unattractive; rather, they sharpen investor focus on programs that can break through the limitations imposed by Medicare’s economics. So, what becomes intriguing to the industry against this backdrop?

Indication Coverage Where Medicare Is Not the Dominant Payer Programs that target cancers or diseases with meaningful prevalence in younger or mixed-age groups tend to preserve stronger pricing and exclusivity conditions. This can include select rare pediatric tumors, niche oncology subsets, metabolic diseases, and certain CNS disorders.

High-Severity Oncology Indications With Clear Willingness to Pay For severe oncology settings where treatment choices are scarce, CMS tends to allow more flexibility and payers apply less resistance. Therapies that deliver clear survival benefits or striking response rates can still achieve premium pricing, even within IRA limits.

Multi-Indication Expansion Potential A small molecule capable of quickly addressing related mutations, additional indications, or expanded lines of therapy can accelerate early revenue before pricing negotiations, enhancing economic value for both biotechs and Big Pharma. In the pan-KRAS example, the compound’s relevance across multiple KRAS mutations and tumor types reinforces the commercial case for its development.

Strong Monotherapy Value Proposition Monotherapies lower treatment costs and streamline clinical uptake, making them appealing to both CMS and private payers. A differentiated small molecule that does not need combination partners can be far more attractive under IRA-driven economic conditions.

Precision-Medicine Stratification Targeted small molecules with companion diagnostics (CDx) can strengthen medical-necessity arguments, sharpen patient selection, and support premium pricing, particularly in oncology. Yet CDx requirements also introduce significant friction: co-development extends timelines, dual regulatory review adds risk, and diagnostic reimbursement is often slower and less certain than drug coverage. Adoption can be gated by test availability and turnaround times, narrowing early patient access and raising commercial execution demands. In short, while a CDx can help defend differentiation, it simultaneously raises the therapeutic’s own barrier to entry technically, operationally, and commercially.

Differentiation That Improves Real-World Utilization Characteristics such as oral delivery, better safety relative to biologics, reduced total care costs, and outpatient administration that lessens healthcare system strain all boost a small molecule’s value within Medicare.

T.Rx’s Perspective

Small molecules remain an important part of our investment strategy, but the bar has shifted as market dynamics have evolved. IRA-related dynamics have pushed many investors, including us, to prioritize opportunities where commercial potential remains despite shorter exclusivity windows. We generally lean towards programs pursuing indications with lower Medicare exposure, clearer pricing durability, and meaningful differentiation relative to existing therapies. Our aim is to back programs that can navigate these pressures while still delivering compelling clinical and economic value. As such, we typically prefer companies pursuing:

Rare diseases primarily affecting patients under 65. These markets are minimally exposed to IRA negotiation and are dominated by commercial insurers, preserving pricing flexibility. Small, genetically defined populations enable faster development, clearer biomarker strategies, and premium pricing supported by high unmet need. Altogether, this is an appealing combination in a compressed exclusivity world.

Non-age-related cancers with commercially insured patient bases (e.g., certain leukemias, sarcomas, or breast cancers in younger adults). These indications avoid Medicare concentration, maintain payer diversity, and typically allow for strong launch economics. Rapid uptake, streamlined reimbursement pathways, and the potential for multi-indication expansion make them compelling for acquirers.

Orphan drugs. Following recent amendments to the IRA, small-molecule drugs approved exclusively for one or more orphan-designated rare diseases are excluded from Medicare price negotiation eligibility, preserving protected pricing and revenue durability. Importantly, the protection is not absolute. If the drug later secures a non-orphan expansion or loses designation, the standard 7-year negotiation clock begins. Still, orphan-only positioning remains one of the clearest remaining structural advantages for small molecules under the IRA, provided indication strategy is tightly managed from the outset.

High-unmet-need indications. In settings where disease severity is high and alternatives are scarce, payers continue to accept premium pricing and rapid uptake, even in small markets or specialized oncology areas. These situations also typically face less pressure from generics and slower competitive entry.

Given IRA-driven constraints on commercial timelines, the strength of IP and clarity of development risk now play a larger role in investment decisions. Our emphasis is on programs that prioritize:

Strong composition-of-matter (CoM) patents, tightly written and filed early;

Credible biochemical and clinical differentiation (potency, safety, durability, or breadth);

Scalable CMC and tractable synthesis, supporting efficient cost of goods and global pricing strategy;

A disciplined indication path that maximizes commercial-payer exposure and avoids Medicare-heavy populations or crowded mechanistic areas.

For founders building preclinical small-molecule therapeutics, the implications are direct:

Prioritize IP early. A strong CoM patent coupled with well-supported MoA-based claims significantly increases optionality, exit value, and partnership interest. Think of IP as a core asset rather than an afterthought.

Demonstrate meaningful differentiation quickly. Investors need to see why your molecule will not simply be another entrant vulnerable to generic erosion or fast-followers, but rather a defensible asset superior potency, safety, durability, or breadth.

Choose indications strategically. Instead of engineering a hammer and then looking for a nail, target indications where the commercial math works from day one: broad reach across large or expanding patient populations, low Medicare exposure, and strong lifecycle leverage.

By aligning molecular differentiation, IP strength, and indication strategy with the evolving reimbursement landscape, founders can continue to build highly investable small-molecule companies, even in a compressed policy environment.

Conclusion

Developing small-molecule therapeutics was once a relatively predictable exercise: compelling biology, clean CMC, a well-designed early-stage trial, and sufficient capital to reach first-in-human data. The IRA has fundamentally reshaped that reality. Exclusivity windows are shorter, pricing pressure is more acute, and large pharma—increasingly sourcing high-quality molecules at low cost from China—has become far more selective about which assets merit downstream investment.

At the same time, the scientific and technological tailwinds are equally profound. Advances in computational chemistry, high-throughput design-make-test-analyze platforms, and modern commercial analytics now allow founders to build clinical differentiation and commercial defensibility into their molecules from day zero. Scientific insight can be directly coupled to market intelligence, enabling precise patient segmentation, competitive positioning, and lifecycle strategy long before a program approaches IND readiness.

In this post-IRA landscape, small-molecule programs succeed not through incremental optimization, but through intentional design. The companies that rise above the noise and secure meaningful venture or pharma engagement are those that embed market alignment, early commercial rationale, and a credible path to durable differentiation directly into their development plans. Increasingly, that means founders are designing reimbursement-aware molecules from the Seed-stage onwards, anticipating access dynamics, payer behavior, and competitive value equations long before entering the clinic. In a constrained biotech environment with a narrower margin for error, only small-molecule programs built on this integrated scientific, development, and economic foundation will earn lasting conviction from investors and partners.

T.Rx Capital Launches $77.5M Fund I to Invest in Bold Startups at the Intersection of Technology and Biology

New venture capital firm to create and invest in early-stage healthcare companies applying novel technologies to frontier biology and redefine patient care

Article

July 12, 2025

Radiopharmaceuticals: The Next Frontier in Precision Cancer Care

Radiopharmaceuticals are emerging as the future of cancer care, combining targeted precision with powerful radiation to deliver safer, more effective treatments.

Article

May 6, 2025

New Non-Opioid Pain Medications: Redefining Relief in the Post-Opioid Era

Biotech companies are racing to develop non-opioid pain medications as safer, effective alternatives to addictive opioids, with breakthroughs like Vertex’s FDA-approved Journavx leading a new era in pain management.

Ready to Transform Healthcare?

Join us in building the future of medicine through innovative technology and biology convergence

.png)